Key Takeaways

- Manual underwriting and monitoring in business lending have become a structural bottleneck — slow, error-prone, and incompatible with modern SME expectations.

- Borrower-side data preparation and lender-side digitisation, structuring and analysis create weeks of delay, force uncertainty surcharges on pricing, and depress conversion.

- Fully data-driven underwriting — built on payment, bank and accounting data — enables short-cycle, precise and explainable credit decisions, with automated collection, standardization, categorization and enrichment. The accounting and ERP data layer, in particular, has been the missing piece for European lenders.

- Post-disbursement monitoring shifts from quarterly check-ins to continuous, signal-based portfolio surveillance, catching covenant breaches and risk drift early.

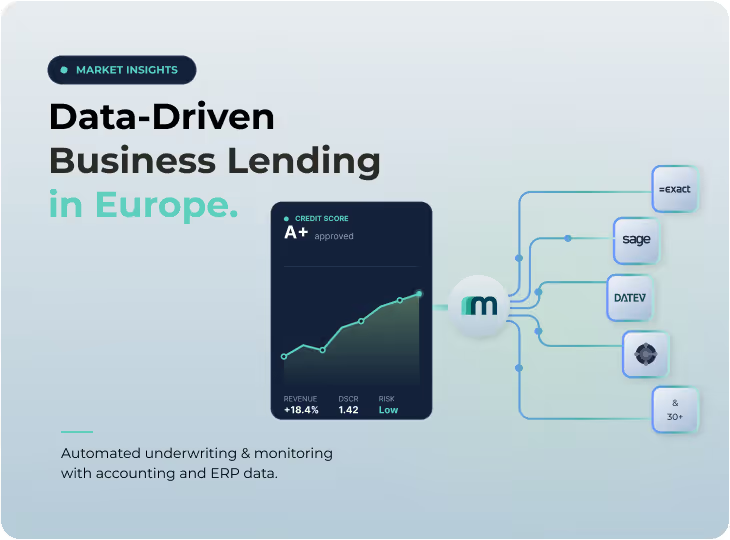

- With Maesn's Unified API, European lenders can source the missing accounting and ERP data from 30+ systems across Europe through a single integration.

The State of Business Lending in Europe: Manual Underwriting Has Reached Its Limit

Across Europe, SME credit demand keeps rising — but most lenders, neobanks and banks still operate underwriting and monitoring stacks designed for a pre-API world. Borrowers email PDFs of their annual accounts, export CSVs from their ERP, screenshot dashboards, and dig through bank statements. Credit teams then re-key, re-format, and re-categorize all of it before analysis can even begin.

The result is a paradox at the heart of business lending: the credit decision depends on financial data, yet the entire process is designed to delay, distort and degrade that data before it ever reaches the underwriter.

For CEOs, CPOs and product owners at lenders, this is no longer a back-office inefficiency. It is a competitive liability.

Why Manual Data Collection and Underwriting Processes No Longer Scale for Lenders

The Borrower Side: Friction Kills Conversion

To get a credit decision, an SME today is typically asked to:

- Gather annual financial statements and reports from their accountant.

- Export transaction lists, debtor and creditor reports from their ERP or accounting system.

- Download bank statements as PDFs or CSVs from multiple accounts.

- Provide management commentary, business plans, and forecasts in unstructured formats.

- Re-submit updated versions every time data is missing, outdated or in the wrong format.

Every additional document is a drop-off point. SMEs increasingly expect the same experience they get from consumer fintechs: connect, decide, disburse. Anything else loses them to a faster competitor.

The Lender Side: Manual Aggregation, Manual Analysis, Manual Risk

On the receiving end, credit operations teams perform tasks that are almost entirely manual:

- Sighting and triage of incoming documents in mixed formats (PDF, XLSX, CSV, paper).

- Digitisation and OCR of statements, with the inevitable misreads and exception handling.

- Restructuring the data into the lender's internal chart of accounts and risk model.

- Categorisation and enrichment of transactions — by hand or with brittle rules.

- Analysis of financial ratios, cash flow patterns and covenant compliance.

This process is:

- Time-consuming. Time-to-decision is measured in days or weeks, not hours.

- Error-prone. Manual re-keying and OCR errors propagate through every downstream model.

- Inconsistent. Two underwriters can structure the same borrower's data differently.

- Expensive. Skilled analyst time is spent on data plumbing instead of credit judgement.

- Risk-distorting. Because the data is incomplete and stale, lenders apply uncertainty surcharges to pricing — costing borrowers, and costing the lender deals to better-informed competitors.

In a market where margins are thin and SME expectations are rising, this model simply does not scale.

Data-Driven Underwriting with Payment, Bank and Accounting Data: The New Standard in Business Lending

The alternative is a fully data-driven underwriting process built on live payment, bank and accounting data, sourced directly from the borrower's systems with their consent.

While payment and bank data are increasingly accessible through open banking frameworks and payment APIs, the accounting and ERP data layer — the source of truth for revenue, margin, receivables, payables, inventory, customer reliabilities and obligations — has remained the hardest piece to access at scale across Europe. The following sections focus on this accounting and ERP data layer in detail.

In a modern, accounting-driven underwriting flow:

- Data collection happens automatically. The borrower connects their accounting or ERP system (DATEV, Lexware Office, Xero, QuickBooks, Sage, Exact, Microsoft Dynamics, Pennylane, Visma, SAP and others) via a one-click consent flow.

- Standardization is automatic. Data from heterogeneous systems is normalized into a single, consistent data model.

- Categorization is automatic. Transactions, accounts and journal entries are mapped to a unified chart of accounts and risk taxonomy.

- Enrichment is automatic. Counterparty data, industry classification, seasonality, customer concentration and cash flow signals are calculated on top of the raw data.

The result: your underwriters receive analysis-ready insights, not raw exports. They spend their time on credit judgement — not on data plumbing or technical integrations.

This unlocks three structural advantages:

- Short-cycle decisions. Time-to-decision drops from weeks to hours, sometimes minutes, for standard cases.

- Precise pricing. Better data quality removes the uncertainty surcharge — pricing reflects actual risk, not data risk.

- Higher conversion. Borrowers experience a frictionless onboarding flow that matches the rest of their digital stack.

For product teams at neobanks and lenders, this is also a foundation for AI-assisted underwriting and automated credit decisioning, which only work as well as the data feeding them.

Automated Credit Monitoring and Portfolio Risk Surveillance After Loan Origination

Underwriting is only the first step. Once credit is disbursed, lenders need to monitor portfolio risk continuously — and this is where manual processes fail most quietly and most expensively.

In a traditional setup, monitoring relies on:

- Quarterly or annual financial statements, often delivered with a 3–6 month lag.

- Email reminders to borrowers to submit updates.

- Manual covenant checks performed by analysts.

- Surprises — usually discovered only when something has already gone wrong.

With data-driven monitoring, the same data pipeline that powered underwriting continues to deliver signals throughout the loan lifecycle:

- Real-time financial KPIs — revenue trends, gross margin, working capital, debt service coverage.

- Cash flow surveillance — sudden drops, late payments, unusual outflows.

- Covenant tracking — automatic checks against contractual thresholds.

- Early warning signals — customer concentration shifts, supplier risk, tax authority activity.

- Portfolio-level analytics — exposure heatmaps and sector trends across all borrowers.

Risk teams move from reactive to proactive. Relationship managers get context before they pick up the phone. And portfolio losses become identifiable months before they crystallise.

Europe's Fragmented Accounting and ERP Landscape: The Real Bottleneck for Data-Driven Lending

In the United Kingdom and the United States, data-driven underwriting is already standard practice. Open Banking in the UK and the maturity of accounting APIs from QuickBooks, Xero, Sage and FreeAgent have given lenders direct access to the source data they need.

Europe is different — and harder. The European business software market is far more fragmented:

- Germany is dominated by DATEV (Unternehmen Online and Rechnungswesen), with significant share for Lexware, sevdesk, Microsoft Business Central, BuchhaltungsButler, Xentral and several others.

- France runs e.g. on Pennylane, Sage, and Cegid.

- The Netherlands uses Exact Online, Twinfield, Moneybird and SnelStart.

- The Nordics rely on Fortnox, Visma e-conomic, Visma Spiris and others.

- Spain and Italy have their own regional leaders, including Sage Active, Holded and many local solutions.

- Switzerland and Austria add bexio, Weclapp and DATEV variants.

For a European lender, building and maintaining a custom integration to each of these systems — with their different authentication models, data structures, business logic and update cycles — is not realistic. It would consume engineering capacity for years and still leave coverage gaps.

This is exactly the gap Maesn closes.

How Maesn's Unified API Enables Automated Underwriting and Monitoring for European Lenders, Neobanks and Banks

Maesn's Unified API for accounting and ERP data gives lenders, neobanks and banks a single, standardized integration to source the borrower's accounting and ERP data from 30+ systems across Europe.

For product and engineering teams at lenders, this means:

- One integration, full European coverage. Connect once, support borrowers on DATEV, sevdesk, Xero, QuickBooks, Sage, Lexware Office, Pennylane, Exact Online, Visma, Fortnox, Microsoft Dynamics 365 Business Central, Odoo, Twinfield and many more.

- A unified data model. Customers, suppliers, invoices, transactions, journal entries, accounts and balances are normalized across systems — analysis-ready out of the box.

- Automated data collection, standardization, categorization and enrichment. Underwriters and risk models consume clean, structured data; not exports, not PDFs.

- Continuous data sync for live monitoring, with webhooks and reliable change detection.

- No data storage architecture, ISO 27001 certification and GDPR compliance — built in Germany, hosted in Europe.

- Stable, maintained connectors. Maesn manages vendor relationships, certifications, API updates and breaking changes — so your team ships credit features instead of maintaining 30+ integrations.

The strategic effect for lenders, neobanks and banks: data ceases to be a bottleneck. Underwriting, pricing and monitoring become functions of how well you model risk — not of how well you can chase PDFs.

From Document-Based Credit Decisions to Real-Time, Data-Native Lending

For CEOs, CPOs and product owners in business lending, the direction of travel is clear. SME credit is becoming a real-time, data-native product. The lenders who win in the next five years will be those who treat borrower data as a live feed, not a quarterly artefact.

That requires three things:

- A decision engine that consumes structured, standardized financial data.

- A monitoring layer that continuously evaluates portfolio risk on the same data pipeline.

- An integration foundation that reliably connects to every accounting and ERP system your borrowers use — across every market you operate in — and combines cleanly with your existing bank and payment data sources.

Maesn provides the third — so your team can focus on the first two.

Talk to our experts to see how Maesn's Unified API powers data-driven underwriting and monitoring across Europe.

About the author

Themo is CEO and Co-Founder of Maesn. With years in strategy consulting — spanning requirements engineering for complex software landscapes, ERP and accounting software selections, and end-to-end integration projects — he holds a Dr.-Ing. with a focus on ERP-to-SaaS transformation. He co-founded Maesn to make system integration effortless.

Co-Founder